Recent buying in foreign stocks has been driven by two factors: performance-chasing after a great year for international stock markets in 2017, and fears that the U.S. stock market is the most overvalued in the world. But if investors think that diversifying their stock portfolio globally will help mitigate the portfolio hit from a plunge in the Dow Jones Industrial Average, they’re wrong.

At least in the short-term, stock market history shows that after a plummeting Dow Jones Industrial Average, the U.S. stock market is more likely to bounce back quickly than foreign stock indexes. For long-term investors, the argument for diversifying overseas remains strong — “set and forget” has the best long-term track record of delivering investment returns. Selling and believing you are smart enough to figure out when to buy again — never a good idea.

It was the size and speed of the move down that caught investors by surprise, but investors should not be taken by surprise if the decline in global stocks lingers.

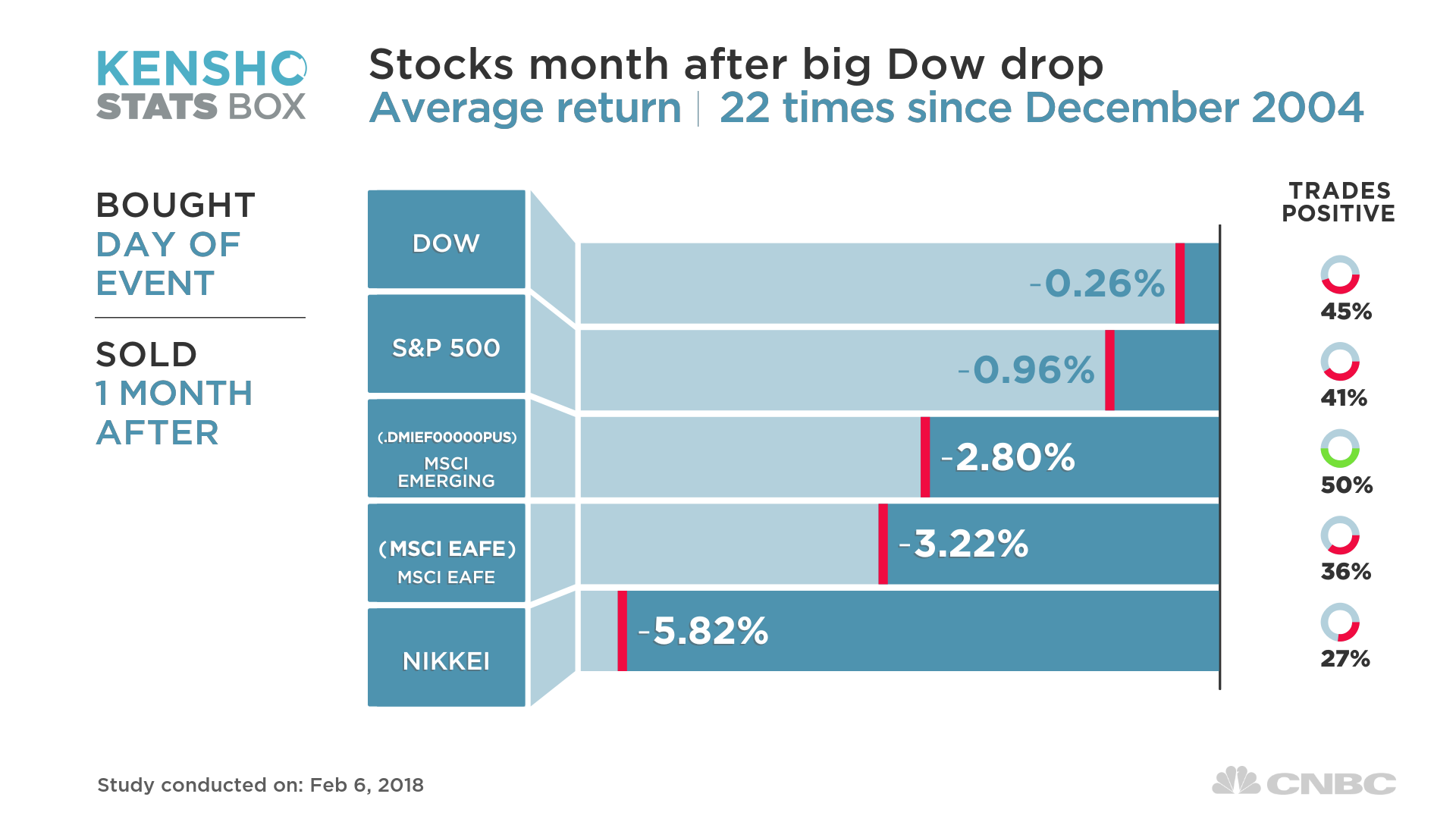

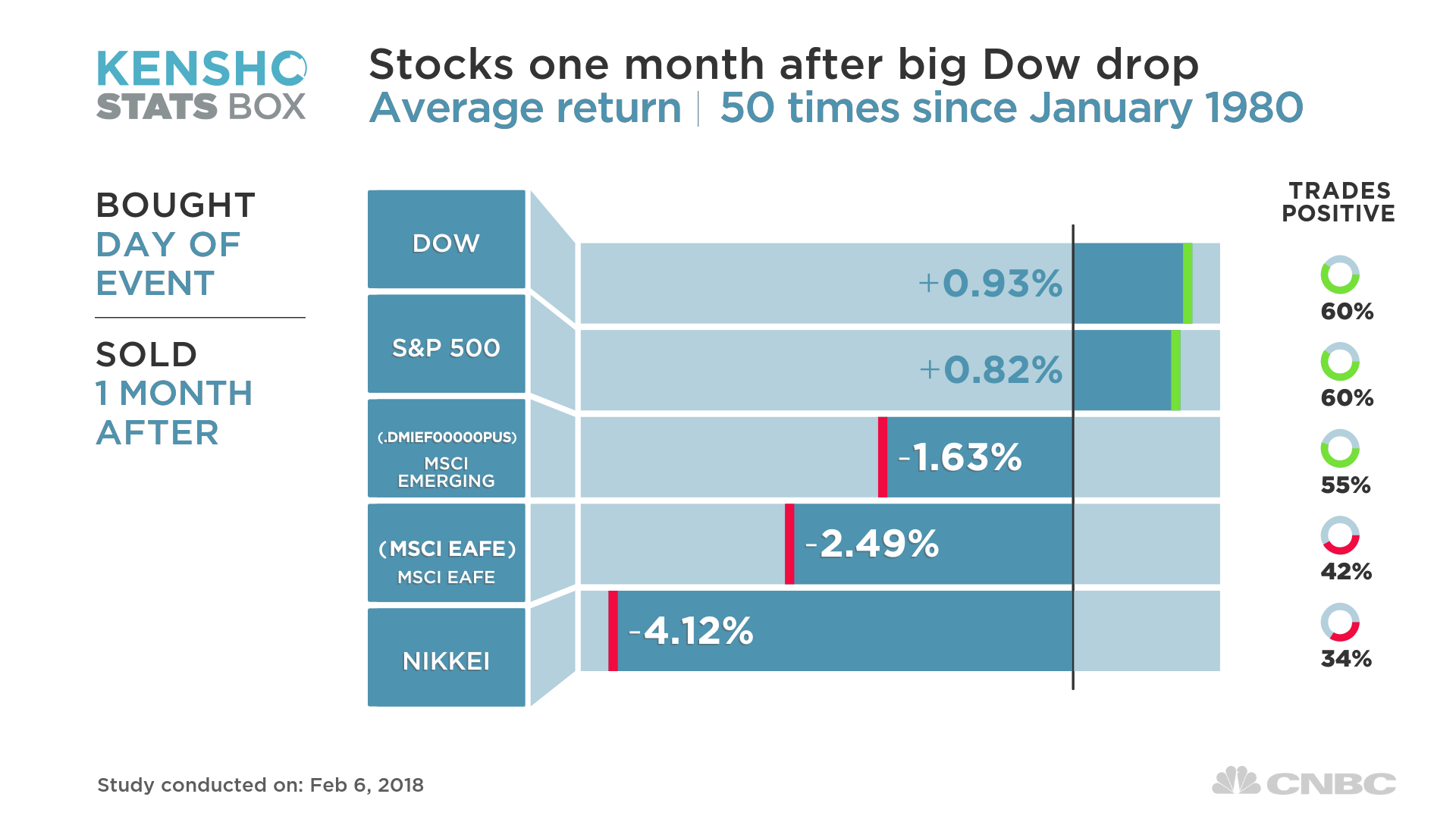

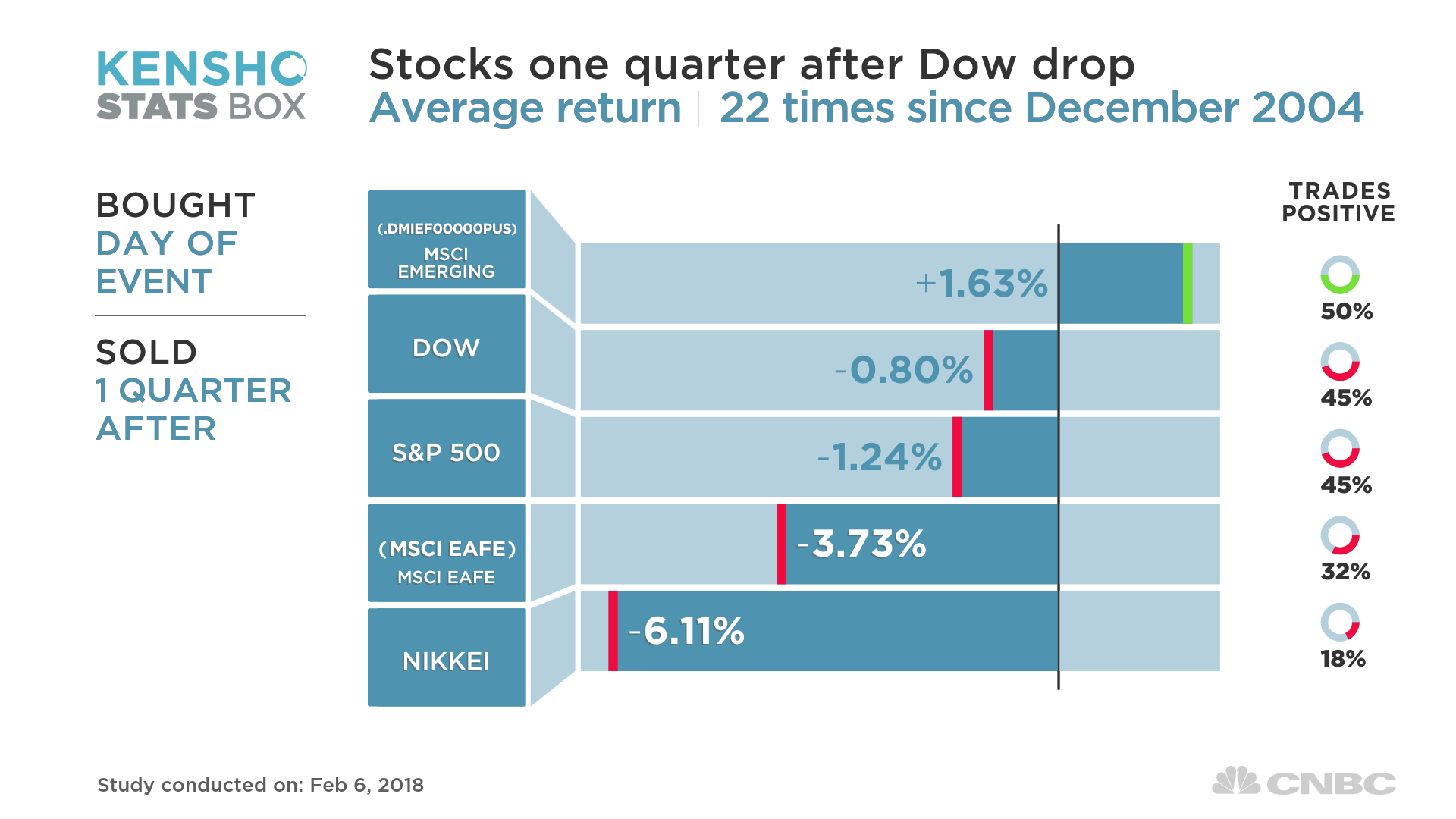

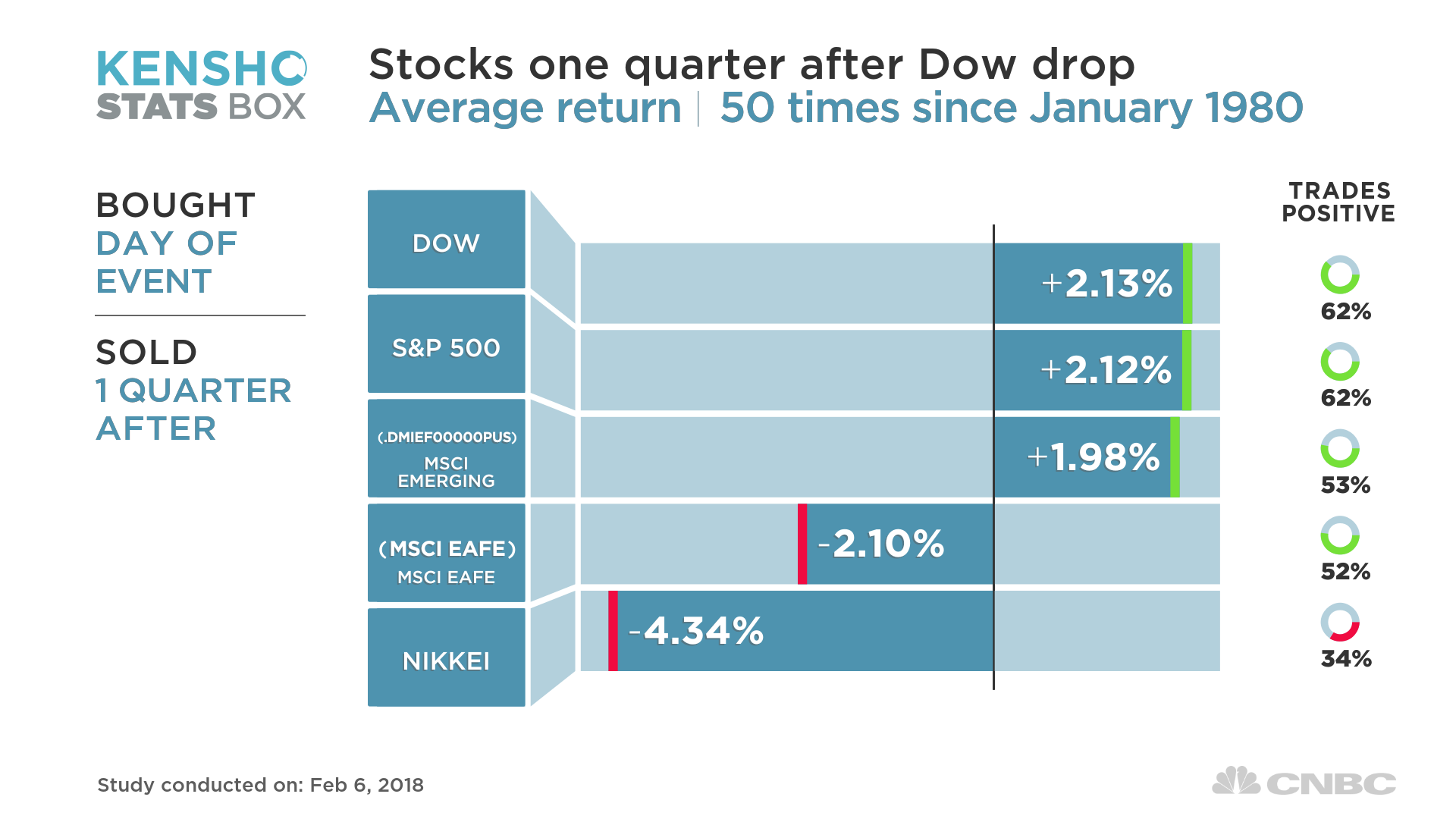

Monday’s Dow plunge was the largest point decline ever, though by the more important measure of percentage decline, it wasn’t nearly as catastrophic. Using Kensho, a hedge fund trading analytics tool, we analyzed the big Dow moves down back to 1980 and, in the more recent period, back to 2004. We limited the screen to Dow declines of at least 6 percent or more that occur in five days or less. Based on the data going all the way back to 1980, U.S. stocks are a much better rebound bet than international stocks. But the picture gets more complicated using the more recent history, back to only 2004.

Here is how two of the flagship international equity benchmarks — the MSCI EAFE Index and MSCI Emerging Markets Index — and the Japanese Nikkei Index react relative to the U.S. stock indexes.

The news gets better a little further out

Home bias is still the norm in stock investing, but even U.S. investors have gotten the international stock bug and are buying overseas markets, especially through ETFs. In January the flows to emerging markets equity ETFs were strong, as were flows to Asia more generally. The iShares MSCI Japan ETF (EWJ) appeared among the top 10 ETFs for new flows in January, taking in more than $2 billion from investors, a spot on the leader board that hasn’t been common for it in recent history. Year-to-date, the four biggest MSCI and FTSE developed markets and emerging markets ETFs have taken in roughly $15 billion from investors, according to XTF.com, which is behind the $20-billion-plus taken in by the three top S&P 500 ETFs, but still notable for retail interest in overseas stocks.

And that’s still the proper way to build a portfolio for the long-term investors — if you’re not in the stubborn camp of Jack Bogle and Warren Buffett, who still resist international diversification.

Both of these indexes bounced back on Tuesday, along with the Dow. But in betting on a rebound from emerging markets or developed markets after a U.S.-led sell-off, the data does show that it’s emerging markets, not developed markets overseas, that have more rebound potential in the following quarter. Emerging markets, in fact, matched or outperformed U.S. stocks in this trading period. While the EAFE, and Japan in particular, were larggards by comparison.

{kind=link}