The financial media tend to focus on a small group of technology companies that are growing rapidly.

But you may want to diversify away from these high-fliers — which include Amazon AMZN, +0.52% and Nvidia NVDA, +1.03% — by investing in large companies with low valuations and attractive dividend yields.

That’s according to Richard Buchwald, a managing director at Logan Capital Management of Ardmore, Pa., which has about $1.9 billion in assets under management for private and institutional clients. The firm runs a variety of strategies, including a concentrated value strategy with $238 million in assets under management as of June 30.

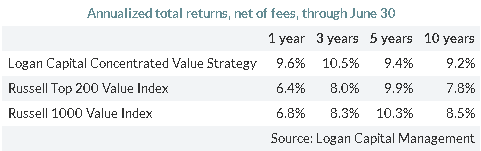

In an interview, Buchwald said decades of experience have shown that “if you put together concentrated portfolios of very-large-cap stocks with sound financials, strong cash flows and balance sheets, over time, the ones with high dividend yields should outperform” the Russell Top 200 Value RT200V, -0.12% and the Russell 1000 Value Index RLV, -0.07%

He said that approach led to less downside when compared with the indexes during periods of significant declines for the U.S. stock market.

Logan Capital Management’s concentrated value portfolio can only be described as highly concentrated, as it typically holds 10 to 15 stocks.

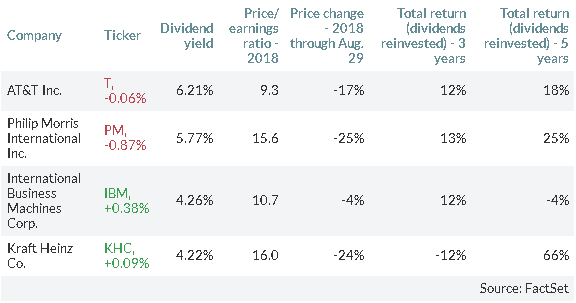

Buchwald discussed four stocks held in the portfolio, which are sorted here by dividend yield:

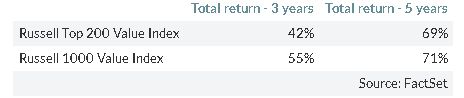

The dividend yields are attractive, but the three-year and five-year returns have not been very good, for the most part, when compared to the two value indexes mentioned above or the S&P 500 Index SPX, +0.01% for that matter:

But that underperformance is part of what makes these four stocks good long-term value investments, according to Buchwald. Here are comments from him about all four:

AT&T

Shares of AT&T T, -0.06% have fallen 17% this year, following a 9% decline in 2017. Those figures exclude the dividend, which is now 6.21%.

Buchwald said the stocks held in the portfolio are “show-me stocks,” with the companies facing challenges to their brands, changes in their markets or transitions as large acquisitions (including AT&T’s June acquisition of Time Warner) are integrated.

But analysts polled by FactSet estimate AT&T’s free cash flow for 2018 will be $21.8 billion, providing plenty of coverage for dividends that Buchwald expects to total about $14 billion.

“Given the financial wherewithal, I can sit and wait for a while,” enjoying the dividends as he waits for a turnaround in the stock price, Buchwald said. He referred to the well-supported dividend as a “cushion” and pointed out that AT&T trades for only 9.3 times the consensus earnings estimate for 2018. That compares to a current-year price-to-earnings multiple of 18.1 for the S&P 500 and 14.6 for the company’s arch-rival, Verizon Communications VZ, -0.69%

Shares of Verizon have a lower dividend yield of 4.32% but the stock “has held up much better because it has not gone through the same transformation AT&T has,” Buchwald said. AT&T acquired DirecTV in July 2015.

Philip Morris International

Philip Morris International PM, -0.87% reported a 12% increase in sales for the second quarter from a year earlier, mainly reflecting an increase in cigarette prices. Cigarette volume sales were down 1.5%. Heated tobacco product sales were up 73% from a year earlier. While these “reduced-risk products” (RRP) made up only 5.5% of total sales during the second quarter, that was up from 3.2% a year earlier.

The company’s second-quarter earnings were up 24% from a year earlier, but when Philip Morris International announced its financial results July 19, it also lowered its sales and earnings targets for all of 2018.

Buchwald said he and his colleagues have “owned [Philip Morris] since we started running this portfolio, in one form or another … over the course of 27 years.” Meanwhile, it has continually raised its dividend and “adapted to a change in environment,” he said.

PMI is making major investments in Japan, where RRP already make up 20% of total sales. Buchwald pointed out that this effort is not going as quickly as the company had hoped, and after Philip Morris executives said as much during their first-quarter conference call on April 19, the shares sank 16% that day.

Buchwald described PMI’s dividend coverage as “tighter.” Analysts polled by FactSet estimate 2018 free cash flow will total $7.5 billion, while Buchwald expects dividends to total $6.8 billion.

IBM

For International Business Machines IBM, +0.38% the official narrative focuses on a transition away from legacy products and services and toward “strategic imperatives,” which include cloud and security software, hardware and services. The company said its revenue from strategic imperatives was up 15% during the second quarter from a year earlier and made up 48% of total sales.

Total quarterly sales were up 4% and gross profits were up 3%.

“The market is looking for some verification” that IBM’s transition will be a success, Buchwald said. “So [during some] quarters they outperform and beat estimates and strategic imperatives will do well, and then the next quarter will be the opposite.”

“But then we look at the financials. We have a stock trading for 10 and a half times earnings with a 4.5% dividend yield,” he said.

Analysts polled by FactSet expect IBM’s free cash flow for 2018 to total $12.2 billion, providing plenty of coverage for the company’s dividend payout of about $5.7 billion.

Buchwald said the low price-to-earnings valuation indicates “a margin of safety” for the stock. “A lot of things have to go right for this to work out well. Meanwhile we are clipping the coupon and hopefully management will get its game plan straight,” he added.

Kraft Heinz

Kraft Heinz KHC, +0.09% is 27%-owned by Berkshire Hathaway BRK.B, -0.49% and 22%-owned by 3G Capital Partners, according to FactSet.

Like many U.S. companies with venerable consumer brands, Kraft Heinz faces increasing competition from producers of lower-cost private label products. This has weighed heavily on the shares over the past two years. But in the second-quarter earnings press release, CEO Bernardo Hees said he believed the company was positioned “to drive sustainable top-line growth from a strong pipeline of new product” and that he expected profitability to improve into 2019.

Analysts estimate the company’s free cash flow for 2018 will total $3.7 billion, compared to dividends of $3.1 billion.

The managers of Kraft Heinz “have proven to be very good at controlling expenses, but they seem to lack, at the moment, any sort of long-term growth,” Buchwald said. “So the market was looking for an acquisition or showing some growth organically.”

“The organic sales decline [of 0.4%] in the most recent report was less than analysts had expected. There was a pretty sharp one-day reaction [after second-quarter results were announced on Aug 3., the shares rose 9% — a gain since given back]. This says that if these guys can actually do what they say, you will get rewarded at some point,” Buchwald said.

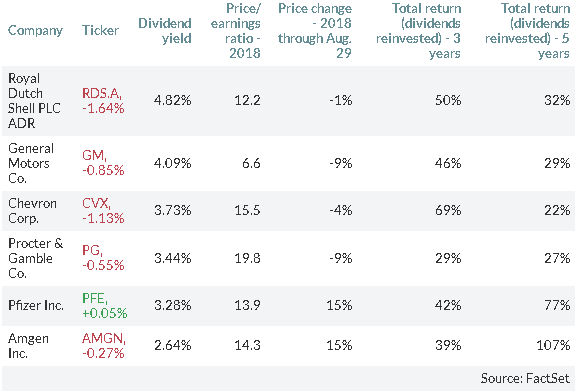

Other companies in Logan Capital’s concentrated value portfolio

Keeping in mind that the portfolio is highly concentrated, usually with only 10 to 15 stocks, each holding will make up between 5% and 10% of the total. So here are six more stocks that were held in the portfolio as of June 30, again ranked by dividend yield:

Portfolio performance

It’s easy to look at the four companies Buchwald discussed and dismiss them because of the challenges they face. But this approach of holding stocks of companies with relatively low price-to-earnings valuations that have attractive dividend yields well supported by free cash flow and strong balance sheets has fared well over time. Here’s how the strategy performed through June against the two benchmarks Buchwald mentioned, according to Logan Capital’s fact sheet for the concentrated value portfolio: