It’s the bane of some older Americans. Once they hit a certain age, the government makes them take money out of their retirement accounts, even if they don’t need the cash.

That is changing, albeit slowly.

The recently passed Secure Act raises the age for when those required minimum withdrawals must begin — to 72 from 70½, effective this year. Meanwhile, updated life expectancy tables proposed by the IRS for 2021 would also change how RMDs are calculated.

“The age change is a small thing, but helpful,” said certified financial planner Mark Wilson, president of MILE Wealth Management in Irvine, California.

And, he said, “Using longer life expectancy calculations would make the minimum amount you have to take a little smaller.”

RMDs apply to 401(k) plans — both traditional and the Roth version — and similar workplace plans, as well as most individual retirement accounts (Roth IRAs do not come with required withdrawals until after the account owner’s death).

Be aware that although the Secure Act raised the RMD age, people who reached age 70½ before 2020 still must take their RMDs. Reach that age after 2019, and you can wait until you’re 72 under the new rule.

“If you reached age 70½ before this year, it’s business as usual for you,” said CPA Jeffrey Levine, CEO of BluePrint Wealth Alliance in Garden City, New York. “Anyone who had to take RMDs before this year has to keep taking them.”

As before, you can delay your first RMD until April 1 of the year following the one in which you reach the RMD age. In all subsequent years you must take the required amount by Dec. 31. If you don’t make those RMDs, you could face a 50% penalty.

However, if you’re working and contributing to a retirement plan sponsored by your employer (and don’t own more than 5% of the company), RMDs do not apply to that particular account until you retire.

The amount you must withdraw is basically determined by dividing the balance of each qualifying account by your life expectancy as defined by the IRS.

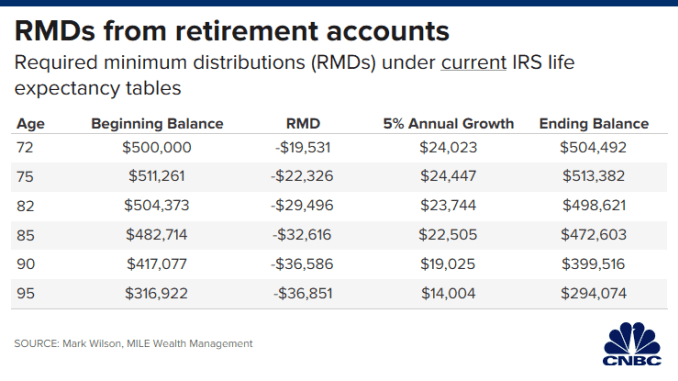

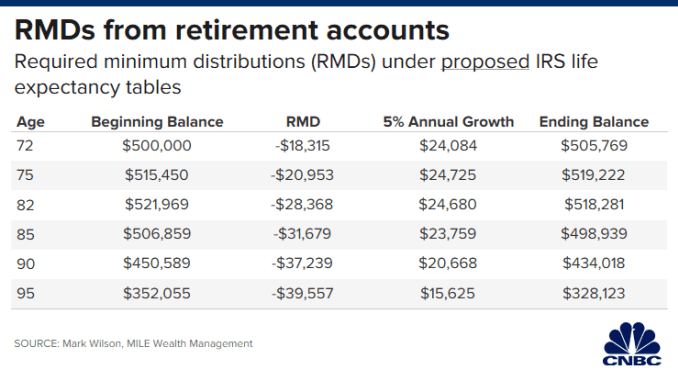

If the agency approves its proposed updated tables, it will mark the first changes since 2002 and could take effect as early as next year. The charts below illustrate how RMD amounts — and account balances — would differ over time, using current life expectancy calculations and the proposed ones.

Be aware that if you were to only take the RMD each year and live at least into your 90s, those minimum amounts would become higher under the proposed new table than under the current one.

Basically, this is due to lower RMDs at the beginning, which leaves more in the account to grow — and higher account balances will eventually result in higher RMDs later in life.

In all, a $500,000 account at age 72, whose only withdrawals are RMDs, would be worth about $34,000 more at age 95 under the proposed life expectancy tables, based on the growth assumptions used in the charts. By that age, though, the RMD would be $3,706 more than under current IRS tables.

Additionally, the Secure Act changed the rules for inherited retirement accounts. Most non-spouse beneficiaries will now have to withdraw the money within 10 years of the original account owner’s death. Before, IRA beneficiaries could stretch withdrawals across many years, based on their own life expectancy.

While RMDs apply whether your assets are meager or massive, most account holders apparently withdraw more, according to the IRS: Just 20.5% are expected to take only the minimum in 2021.

“The only people who take just the minimum are the ones who don’t need the money,” said Ed Slott, CPA and founder of Ed Slott and Co. in Rockville Centre, New York.

He added that if you can afford to delay withdrawals, however, the higher RMD age will be helpful.

“Those people can wait a little longer, and the icing on the cake will be the new tables giving them increased life expectancy so they can take a little less out,” Slott said.

Also, a later RMD age potentially could provide extra time to do some tax planning to minimize the impact of those withdrawals when you do need to take them.

For example, some advisors recommend moving money to a Roth IRA from a traditional IRA or 401(k). While you’d have to pay taxes on the amount converted, you’d pay no taxes on those Roth withdrawals down the road. And, you can spread that conversion over several years to minimize the annual tax impact.