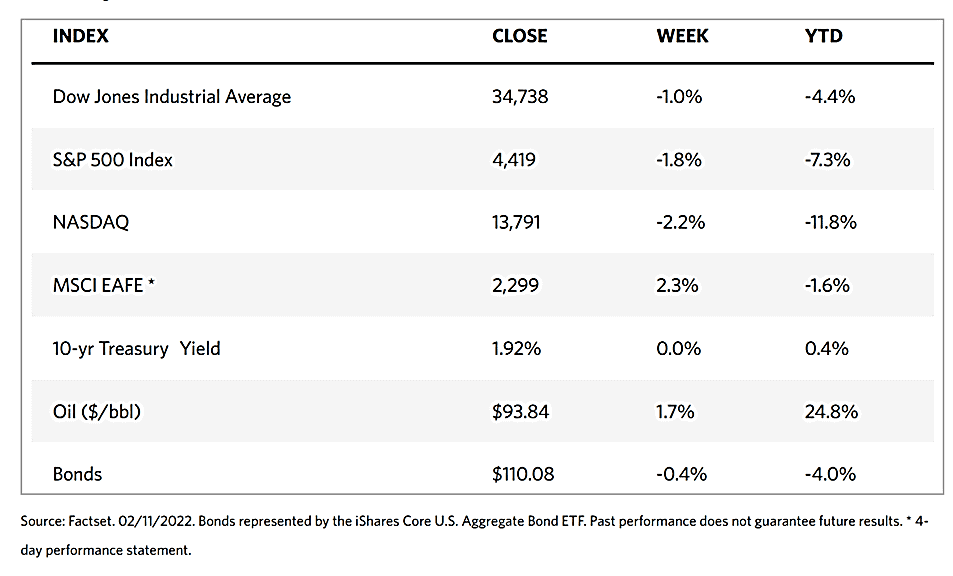

Stock Markets

Volatility marked this week’s trading which saw large-cap indexes end lower and the S&P MidCap 400 and small-cap Russell 2000 indexes treading water with modest gains. Underperforming the rest was the technology-laden Nasdaq Composite Index that ended the week down 15% from its recent high and ending in correction territory. Investor sentiment continues to be dominated by the clash between robust earnings growth and worries about the impending monetary tightening. The possibility of a Russian invasion of Ukraine overshadows speculations, causing a sell-off at the week’s end. Pulling down the broader indexes early in the week were declines in the large-cap technology stocks such as Google parent Alphabet, Facebook parent Meta Platforms, and Microsoft, although lost ground was recovered by the middle of the week. Counters in the hospitality sector such as hotels, restaurants, casinos, online travel agencies, and air and cruise lines rallied with the continued opening of the economy.

U.S. Economy

On Thursday, it was announced that the inflation rate hit its highest level in forty years, jarring the markets and erasing the gains made by midweek. News released by the Labor Department showed the consumer price index (CPI) surged 7.5% for the year ending January. This is higher than consensus expectations, and topped annual gains going back to February 1982. Core prices not including food and energy purchases climbed 6.0%, the highest since August 1982. Due to concerns about inflation, the University of Michigan reported that the preliminary benchmark for consumer sentiment came in at 61.7, well short of the expected 67 and the lowest it has been since October 2011.

The announcement of the upper-limit CPI and comments about more restrictive monetary policies by James Bullard, St. Louis Federal Reserve Bank president, propelled short-term rates upward on Thursday resulting in a flattening of the yield curve. As investors priced in a Fed rate hike accelerated schedule, the two-year U.S. Treasury note yield ascended to its highest point in two years. Investors included the plausible scenario of a 50-basis-point rate hike by the Fed’s policy meeting in March. The benchmark 10-year U.S. Treasury note yield exceeded 2.00% for the first time since mid-2019.

In the underlying fundamentals, there appears to be broad-based resiliency across goods and services. Price pressures are spreading beyond a few items that are still affected by supply-chain disruptions, resulting in higher food, electricity, used cars, and housing prices which led to price hikes. The most significant component in the consumer-spending basket, rents, is likely to accelerate further as a result of rising home prices, a tight labor market, and the lowest rental vacancy rate in 38 years. A descent to more moderate price increases is unlikely to take place soon with the services inflation picking up. This might prompt central banks to take more aggressive measures moving forward. The good news, however, is that GDP is expected to continue growing at an above-average pace for the year and the unemployment rate will remain at near-record lows. The economy does not need further support. The expected increases in interest rates will increase the cost of borrowing that may in turn temper consumer spending, thus balancing off supply and demand, slowing down inflation.

Metals and Mining

There is a breakout in gold prices above the $1,850 critical resistance level, closing the week at a three-month high. As tensions heightened between the U.S. and Russia, causing gold to surge late Friday. Triggering the rally was the White House announcement that recommended all U.S. citizens to leave Ukraine within 48 hours. The news sparked a 500-point sell-down in the Dow Jones Industrial Average for a 1% drop for the day. Simultaneously, gold gained 1% for the day, trading last at $1,863.80 per ounce. The continued volatility in equities is only seen to further help the precious metals market see substantial gains. When there is a lot to fear in the financial markets, gold becomes more attractive as a stable safe haven.

Gold gained 2.79% last week, from the earlier week’s close at $1,808.28 to the just-concluded week’s close at $1,858.76 per troy ounce. Silver, formerly at $22.52 ascended to close at $23.59 per troy ounce for a gain of 4.75%. Platinum rose slightly from $1,028.19 to $1,030.80 per troy ounce, an increase of 0.25%. Palladium also climbed from $2,294.06 to $2,308.50 per troy ounce to record a 0.63% price appreciation. Among the base metals, copper price increased from the previous week’s $9,841.50 to this week’s close at $9,860.50 per metric tonne, increasing by 0.19%. Zinc inched up 0.39% from $3,612.50 to $3,626.50 per metric tonne as aluminum climbed 2.03% from $3,074.00 to $3,136.50 per metric tonne. The price of tin went up 1.23% for the week, from $43,021.00 to $43,549.00 per metric tonne.

Energy and Oil

Over the past week, Iran was front and center in the oil market news, on the back of a potential breakthrough in the nuclear deal. Negotiations were expected to be successful by several market participants, resulting in oil prices descending over the week as a correction to the previous week’s climb to the mid-$90s per barrel. Even if a deal were to take place soon, it would take several months before Iran’s crude oil to reach the markets; thus, the sudden and unexpected rally was driven more by market optimism rather than realistic expectation. Taking a closer look at fundamentals, the underperformance of OPEC+ appears to suggest levels close to one million barrels per day (b/d) in February. The rumors have even prompted the International Energy Agency (IEA) to weigh in for more oil production. The IEA joined the ranks of countries such as India as well as other major importers in calling for OPEC+ to raise the supply in the crude market. The Agency urged Saudi Arabia and the United Arab Emirates to use their spare capacity to supplement the deteriorating underperformance of OPEC+. Volume shortage has totaled some 800,000 b/d since the beginning of 2021. As if to add to the supply problem, global shortages of diesel have become more pronounced as Northwest Europe inventories descended to their lowest level since 2008 at least. Singapore gasoil stocks have also fallen to multi-year lows of approximately 8.2 million barrels.

Natural Gas

For the report week February 2 to February 9, spot prices for natural gas fell at most locations. The Henry Hub spot price descended from $6.44 per million British thermal units (mmBtu) at the start of the week, to $4.06/mmBtu by the end of the week. International natural gas prices also fell in the global market. The March 2022 NYMEX contract price dropped $1.492 to $4.009/mmBtu to $5.501/mmBtu week-on-week. The price of the 12-month strip-averaging March 2022 through February 2023 futures contracts slipped $1.019 to $4.174/mmBtu. All along the Gulf Coast, prices for natural gas fell as the effects of the cold front dissipate across Texas. The drop in the prices in the Midwest corresponded with the Henry Hub price, even as prices fell in the West in response to the rising temperatures. The U.S. total natural gas supply fell during this report week due to decreased dry natural gas production. The total consumption of natural gas throughout the U.S. fell in line with decreased consumption in most sectors, while LNG exports are up by five vessels this week from last week.

World Markets

In Europe, share prices rallied on the back of strong corporate earnings. The pan-European STOXX Europe 600 Index closed 1.61% higher in local currency terms. The value-oriented stocks and cyclical industry stocks performed better compared to the market. This is seen to be in reaction to the inflationary pressures and the likely implications they have for the monetary policy initiatives of major central banks. Germany’s Xetra DAX Index surged 2.16%, Italy’s FTSE MIB Index climbed 1.36%, and France’s CAC 40 Index rose 0.87%. The UK’s FTSE 100 Index advanced 1.92%, buoyed by positive investor reaction to better-than-expected economic data. The core peripheral eurozone government bond yields ascended in response to the higher-than-expected inflation forecast announced by the European Commission and an unexpected rise in U.S. inflation. After data was reported that the economic contraction was below expectations in December and grew 1% in the fourth quarter, UK gilt yields increased. The resilience demonstrated by the markets prompted investor expectations that the Bank of England may soon increase interest rates again. Overall, the EC lowered its 2022 outlook for EU economic growth from its previous forecast of 4.3% to 4.0%.

Despite last week being a holiday-shortened week for Japan, its stock markets posted gains as the Nikkei 225 Index rose 0.93% and the broader TOPIX Index climbed 1.66% in response to solid corporate earnings. The yen lost some of its value against the U.S. dollar, weakening to approximately JPY 116.02 from what was previously JPY 115.22. The higher-than-expected U.S. inflation rate sent the foreign currency upwards in response to expectations of a move by the Federal Reserve to aggressively tighten their monetary policy. The ten-year Japanese government bond yield ended the week at 0.22%, a 10% increase from the 0.20% at the end of the previous week, prompting the Bank of Japan to quickly move to curb rising yields and to ensure a more stable and favorable financial situation. BoJ Governor Haruhiko Kuroda continued to assure the market that monetary policy will remain at its current trajectory since inflation in Japan remains well below its 2% target.

Chinese equities gained on official assurances of support and a perception that the regulatory crackdowns by authorities have peaked. The Shanghai Composite Index added 3% in value while the CSI 300 Index gained 0.8% since January 28, the final trading day prior to the weeklong Lunar New Year break. In the past week, the People’s Bank of China (PBOC) announced that loans for affordable rental housing would not be included in the limited amount banks may lend to the property sector. In the Communist Party newspaper People’s Daily, an editorial stated that China’s economy still needed capital for growth despite requiring regulations on the use of capital to curb the tendency towards monopolistic behavior. It was also stated in another article that regulatory control on the internet sector will become increasingly rules-based, suggesting a possible easing of the government’s crackdown on the tech sector. PBOC data indicated that the country’s foreign currency reserves dropped in January by approximately $28 billion to $3.22 trillion. This is lower than expected during a month that saw the U.S. dollar strengthen. New loans and aggregate financing exceeded forecasts, rising to record levels in January, according to the central bank. China’s credit growth will possibly accelerate in the months to come amid reductions in borrowing costs, a more accommodative fiscal policy, and the relaxing of constraints on mortgage lending.

The Week Ahead

Among the vital economic data to be released in the coming week are the Leading Economic Indicators index and Industrial Production.

Key Topics to Watch

- Louis Fed President James Bullard interviewed

- Producer price index

- Empire State manufacturing index

- Retail sales

- Retail sales excluding autos

- Import price index

- Industrial production

- Capacity utilization

- Business inventories

- NAHB home builders’ index

- FOMC minutes

- Initial jobless claims

- Continuing jobless claims

- Building permits (SAAR)

- Housing starts (SAAR)

- Philadelphia Fed manufacturing index

- Louis Fed President James Bullard speaks

- Cleveland Fed President Loretta Mester speaks

- Chicago Booth School – New York Fed meetings

- Existing home sales (SAAR)

- Leading economic indicators

- Fed Gov. Christopher Waller speaks

Markets Index Wrap Up