Stock Markets

Markets tread water throughout the week in anticipation of the Federal Reserve’s annual symposium in Jackson Hole, Wyoming, held from August 22 to 24. While there are typically no policy decisions made at this meeting, the Jackson Hole Symposium influences global financial markets. Expectations about interest rates and monetary policy are shaped by pronouncements by the Fed, particularly those articulated in Jackson Hole. The stock market has been fixated for a long time on the timeline of rate cuts, and the policymaking body has held its policy rate unchanged for more than a year. Fed Chair Powell’s speech on Friday suggests that officials perceive that the central bank’s dual mandate of stable inflation plus maximum employment has been sufficiently met to begin adjusting rates.

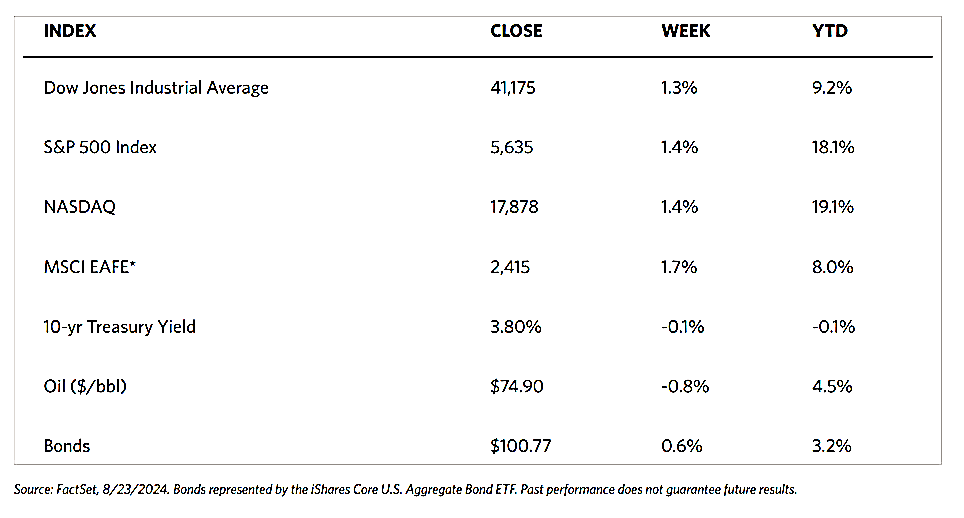

All major U.S. stock indexes are up for the week. The Dow Jones Industrial Average (DJIA) rose by 1.27% while the Total Stock Market Index outperformed by climbing 1.65% for the week. The S&P 500 Index advanced by 1.45% which is not far from the technology-heavy Nasdaq Stock Market Composite’s 1.40% gain. The NYSE Composite Index rose by 1.81% with all Russell components up. The CBOE Volatility Index (VIX), the indicator of investor risk perception, also went up by 7.16%. The rising stock market is therefore viewed as accompanied by rising volatility risk.

U.S. Economy

The economic news released this week came in mostly aligned with expectations and did little to move the markets. The S&P Global report on its first estimate of August economic activity confirmed that the manufacturing sector remained in a slump. It also confirmed, however, that the larger services sector continued at a healthy rate of expansion. Existing home sales rose slightly and in accordance with expectations, ending four months of straight declines. There was, however, the unexpected announcement by the Labor Department in its annual revision of its nonfarm payroll count through March. The estimates were revised downward by 818,000 jobs over the previous 12 months than were originally reported. The July jobs report was underwhelming because monthly hiring slowed and the unemployment rate inched up to its highest level since October 2021. A few weeks ago, this triggered recession worries and sparked the early August market drop. The recession panic seems to be overblown, and the data in recent weeks turned out to support a more positive outlook.

Metals and Mining

While gold ended last week above $2,500, it was uncertain if it would correct this week below that resistance level. Gold ended this week solidly above that level, making it a support level for the metal’s further upward movement. It is trading near record highs and signaling strongly that this latest rally is not over. There appears to be no signs of the market overheating albeit being hot, nor are there signs of frothy volatility that it may be approaching its peak. Gold seems to have plenty of room to rally as the Federal Reserve is just beginning a new easing cycle, according to analysts. The Fed dispelled any doubts that rates will be coming down in September. The minutes from the July monetary policy meeting indicated that several committee members were in favor of lowering the Fed Funds rate last month. This may negatively impact the U.S. dollar, rendering the USD index at a low for the year, breaking below 101 points. A weak dollar and low rates create a favorable situation for precious metals. Furthermore, other precious metals critical to the electrification of the global economy may turn bullish.

The spot prices of precious metals rose for the week. Gold modestly advanced by 0.18%, from its close last week at $2,508.01 to its close this week at $2,512.59 per troy ounce. Silver closed last week at $28.98 but ended this week at $29.82 per troy ounce for a gain of 2.90%. Platinum ended one week ago at $957.20 and this week at $965.62 per troy ounce, rising by 0.88%. Palladium ended this week at $964.30 per troy ounce, up 1.35% from its end last week at $951.48. The three-month LME prices of industrial metals were also up for the week. Copper, which ended last week at $9,115.50, closed this week at $9,288.50 per metric ton for a weekly gain of 1.90%. Aluminum last traded one week ago at $2,365.50 and this week at $2,542.00 per metric ton to register a gain of 7.46%. Zinc closed this week at $2,912.00 per metric ton, an increase of 5.41% over last week’s close at $2,762.50. Tin ended this week at $32,912.00 per metric ton for a 3.16% gain over last week’s close at $31,903.00.

Energy and Oil

This week, oil prices remained rangebound. The market appears to be recovering after the frenzy in the first two weeks of August. ICE Brent settled in a narrow band between $76 and $78 per barrel. After the US Federal Reserve’s July meeting notes indicated September would be the most probable date for the Fed interest rate cut, overall sentiment in the oil market has been improving. Macroeconomics might lift oil even higher if the Federal Reserve’s symposium at Jackson Hole does not disappoint.

In the meantime, a megamerger of two leading U.S. coal producers creates a new industry giant. Major coal producers Arch Resources and Consol Energy will merge in an all-stock deal to create a mining giant valued at more than $5 billion. It will boost an export capacity of 25 million tons per annum across two separate shipping terminals.

Natural Gas

For the report week beginning Wednesday, August 14 to Wednesday, August 21, 2024, the Henry Hub spot price fell by $0.05 from $2.17 per million British thermal units (MMBtu) to $2.12/MMBtu. Concerning Henry Hub futures, the price of the September 2024 NYMEX contract decreased by $0.042, from $2.219/MMBtu last Wednesday to $2.177/MMBtu yesterday. The price of the 12-month strip averaging September 2024 through August 2025 futures contracts declined by $0.041 to $2.978/MMBtu. At most locations, natural gas spot prices fell, ranging from a decrease of $0.47 at the Waha Hub in West Texas to an increase of $0.39 at Northwest Sumas on the Canada-Washington border.

International natural gas futures price changes were mixed this report week. The weekly average front-month futures prices for liquefied natural gas (LNG) cargoes in East Asia increased by $1.27/MMBtu to a weekly average of $13.90/MMBtu. Natural gas futures for delivery at the Title Transfer Facility (TTF) in the Netherlands, the most liquid natural gas market in Europe, decreased by $0.16 to a weekly average of $12.60/MMBtu. In the week last year that corresponds to this report week (beginning August 16 and ending August 23, 2023), the prices were $14.09/MMBtu in East Asia and 12.35/MMBtu at the TTF.

World Markets

The pan-European STOXX Europe 600 Index closed this week higher by 1.31% on the back of rising hopes for interest rate cuts by both the Fed and the European Central Bank (ECB) by September. The major continental stock indexes also closed higher. Italy’s FTSE MIB gained by 1.83%, France’s CAC 40 Index advanced by 1.71%, and Germany‘s DAX added 1.70% for the week. The UK’s FTSE 100 Index gained by 0.20%. Eurozone business activity was boosted by the Paris Olympics, although manufacturing is still shrinking. Eurozone business activity stalled in July but picked up in August, as suggested by the S&P Global purchasing managers’ index (PMI). The Olympic games in France drove the services sector to a four-month high, as the first estimate of the HCOB Eurozone Composite PMI Output Index came in at 51.2 from 50.2 (a reading greater than 50 signifies expansion). However, manufacturing production contracted for the 17th consecutive month. According to the ECB, growth in negotiated wages in the eurozone (a key indicator for monetary authorities) slowed to 3.55% in the second quarter, down from 4.74% in the three preceding months. In its August report, the Bundesbank said that “the expected slow recovery in the [German] economy is being delayed further” by weak foreign demand.

Japan’s stock markets rose modestly for the week. The Nikkei 225 Index moved upward by 0.8% while the broader TOPIX Index inched up by 0.2%. Bank of Japan (BoJ) Governor Kazuo Ueda reiterated that the central bank would continue to normalize its monetary policy as it gains confidence that the economy may achieve 2% inflation in a stable manner, amid some speculation that recent market turmoil could discourage the Bank of Japan (BoJ) from further hiking interest rates. For the third straight month in July, core consumer price inflation accelerated, supporting the BoJ’s hawkish shift this year. The yen strengthened to the high end of the JPY 145 against the USD range from about JPY 147.6 at the end of the previous week, amid contrasting monetary policy outlooks for Japan and the U.S. The yield on the 10-year Japanese government bond rose from the prior week’s 0.88% to this week’s end at 0.90%. the latest domestic inflation data was aligned with the BoJ’s conservative shift. The nationwide rate of core consumer price inflation climbed to 2.7% year-on-year from 2.6% in June, in line with expectations. The headline rate of inflation remained unchanged at 2.8% year-on-year. In terms of GDP growth and consumption, broader domestic data appear healthy.

Ahead of Fed Chair Powell’s Jackson Hole speech and on the back of a light economic calendar, Chinese stocks fell as buyers were kept on the sidelines. Both the Shanghai Composite and CSI 300 Indexes declined for the week, although the Hong Kong benchmark Hang Seng Index advanced. China’s central bank kept its benchmark lending rates unchanged on Monday, a reflection of policymakers’ intention to protect banks’ profit margins. The People’s Bank of China (PBOC) maintained the one-year loan prime rate at 3.35% and the five-year loan prime rate (LPR) at 3.85%. The LPR is a policy rate for mortgages and other long-term loans. After the bank unexpectedly trimmed several key rates in July, economists broadly expected the PBOC’s decision to remain steady on both LPRs. However, it is believed that there is room for further loosening in China this year should the Fed start cutting rates in the U.S. In earnings releases, the search engine leader Baidu’s second-quarter revenue came in lower than expected, even though earnings beat analysts’ forecast. Baidu, based in Beijing and often referred to as China’s Google, reported that second-quarter revenue ending June dropped by 0.4%.

The Week Ahead

Among the important economic releases scheduled in the coming week are personal income and spending for July, the second quarter GDP, and July inflation data.

Key Topics to Watch

- Durable-goods orders for July

- Durable-goods minus transportation for July

- San Francisco Fed President Daly TV interview (August 26)

- S&P Case-Shiller home price index (20 cities) for June

- Consumer confidence for Aug.

- Atlanta Fed President Raphael Bostic speech (August 28)

- Initial jobless claims for Aug. 24

- Advanced U.S. trade balance in goods for July

- Advanced retail inventories for July

- Advanced wholesale inventories for July

- GDP (2nd revision) for Q2

- Pending home sales for July

- Atlanta Fed President Raphael Bostic speech (August 29)

- Personal income (nominal) for July

- Personal spending (nominal) for July

- PCE index (for) July

- PCE (year-over-year)

- Core PCE index for July

- Core PCE (year-over-year)

- Chicago Business Barometer (PMI) for Aug.

- Consumer sentiment (final) for Aug.

Markets Index Wrap-Up