It’s common to think about the importance of cash at the onset of weather emergencies like Hurricanes Helene and Milton. At the same time, people who are evacuating in anticipation of natural disasters or working to repair homes and neighborhoods in the aftermath also need digital access, as reinforced by the Atlanta Fed’s Katrina’s Classroom curriculum.

In previous Take On Payments posts, we’ve discussed the importance of having access to cash as well as the ability to use digital payments in times of crises. This gets to the concepts of being fully served and underserved in digital payments. You might be asking what exactly these terms mean. Sometimes when we talk about these concepts, it can feel like an “I know it when I see it” situation.

A new research paper by authors at the Federal Reserve Banks of Atlanta, Boston, and Kansas City, and the Federal Reserve Board of Governors aims to clear up this ambiguity. Specifically, the goal of the paper is to define households that are fully served and underserved in the digital payments services space by using quantitative data as a foundation for evaluating efforts to improve access.

Building on research in the US and other countries, the paper proposes ways to evaluate four aspects of being fully served: access, use, safety, and affordability.

Access: This is defined as the ability to use at least one of the following types of transaction methods digitally: bank accounts, nonbank online payment services, prepaid cards, and credit cards. “Access” is defined more broadly than “banked” (someone who uses traditional banking services). Most US households have access.

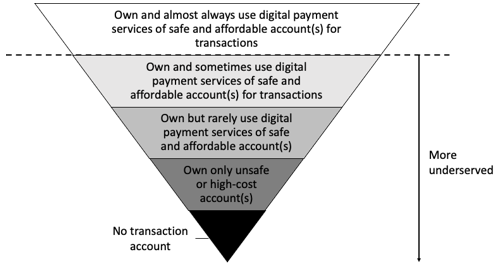

Use: Whether or not, and to what degree, a household uses safe and affordable digital payments indicates how well served the household is. The figure below, simplified from the paper, shows the continuum from fully served to unserved households.

Safety: The paper identifies four components of safety: avoidance of theft and loss, disclosure of terms and conditions, fair treatment and business conduct, and data privacy and protection.

Affordable: Direct costs, including account fees and per-transaction fees, and indirect costs like transportation and internet or mobile services are included in affordability. Cash, while rated as low-cost by consumers, involves indirect costs that are difficult to measure. A more practical proxy would be a certified Bank On![]()

The paper also identifies data gaps for understanding digital payments exclusion. At one end of the spectrum, it suggests using qualitative studies. On the other end, it recommends using big data to gain insights into the motivations and behaviors of underserved households. Moving away from “I know it when I see it” and toward measurement is an important step to making every household fully served in digital payments.