Container import demand (IOTI) has collapsed over the past month, joining the truckload (OTVI) market in posting double-digit year-over-year declines. Intermodal (ORAILL) has remained relatively resilient, but given its close ties to import volumes, it may not be far behind.

Uncertainty continues to dominate business decision-making, as companies remain impacted — directly or indirectly — by erratic trade policies and the rhetoric surrounding them. While this market has been anything but predictable, current indicators point to a relatively soft second half of 2025. Let’s walk through the supply chain to understand why.

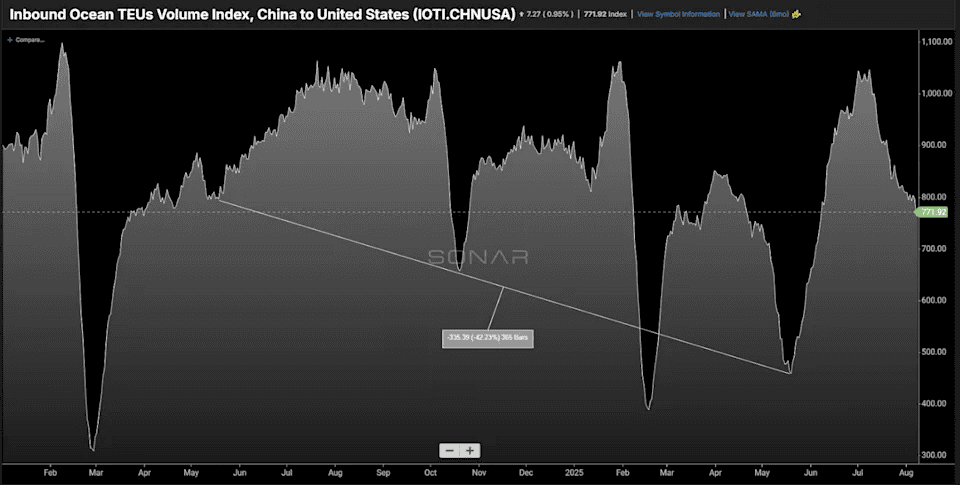

Seasons shift

The trade war has disrupted traditional seasonal freight patterns, and nowhere is that more evident than in the import sector. Aggressive tariff threats and implementations have prompted shippers to pull orders forward in an effort to avoid higher duties.

In April, a 145% tariff on Chinese goods led to a 42% drop in containerized import bookings from China to the U.S. Since China accounts for over 30% of all containerized imports to the U.S., this has had a disproportionate impact on the domestic freight market.

This sharp drop in imports had minimal effect on the already deflated truckload market, which has lost most of its long-haul share to intermodal. However, it did noticeably impact intermodal volumes, which were down a modest 5% year-over-year in early June.

Once the tariff was paused, ordering resumed at a rapid pace, peaking in late June and early July before falling off again. Traditionally, the peak season for container imports occurs in late July and August as retailers prepare for the holidays. This year, much of that activity appears to have happened one to two months early.

What that means for intermodal

Intermodal typically peaks in September and October. However, the early surge in imports suggests we could see an earlier-than-usual intermodal peak — particularly for international containers.

Still, the latest Logistics Manager’s Index (LMI) report offers a counterpoint: inventories are currently being held upstream to avoid the higher costs of storing goods closer to the end consumer. This strategy could lead to a more spread-out or “diffused” intermodal peak, with international volumes moving earlier and domestic movements occurring closer to the traditional time frame.

Several carriers have already announced peak season surcharges for September, which could accelerate some freight movement if capacity allows.

The trucking market is likely to continue its slow burn as capacity exits unless demand unexpectedly spikes. For now, consumption remains sluggish, giving shippers ample lead time to manage inventory replenishment.

A few wild cards

Hurricanes could temporarily disrupt freight networks, but recent years have shown that winter weather events have a more lasting impact.

Holiday shipping may be chaotic if shippers are caught flat-footed. The ongoing uncertainty may leave businesses without a clear sense of consumer demand, forcing them into reactive logistics strategies. With leaner networks and less buffer in capacity, even small disruptions could snowball into panic.

The broader economy remains the most unpredictable variable. While interest rate cuts, tariff deals, tax breaks, or other incentives could jumpstart investment, a significant economic rebound in 2025 still appears unlikely.