Oil gave up earlier gains and fluctuated after the Wall Street Journal reported that the International Energy Agency is proposing a record release of reserves to tackle elevated prices triggered by the Iran war.

The release would exceed the 182 million barrels that IEA members put into the market in 2022 after Russia invaded Ukraine, according to the newspaper. Brent slipped to trade around $88 a barrel after rising as much as 3.7%, while West Texas Intermediate swung near $84, continuing a period of extreme market volatility this week that saw prices punch above $100 on Monday.

The effective halt to shipping through the Strait of Hormuz, the narrow channel that typically handles a fifth of global oil flows, has led to major Gulf producers cutting output and driven up prices of crude, natural gas and products such as diesel. Tanker traffic across the waterway has dwindled to a trickle and the market is keenly watching for a resumption of normal trade.

IEA members are expected to decide on the proposal to release emergency reserves on Wednesday, the WSJ said, citing officials familiar with the matter. The measure would be adopted if none object, but protests by one country could delay the plan, it said. The Group of Seven nations had earlier this week asked the IEA to prepare scenarios for the release of emergency oil stockpiles.

A release by the IEA “is both a relief valve and a warning signal,” said Charu Chanana, chief investment strategist at Saxo Markets in Singapore. “It can add temporary supply and cap panic, but it also tells the market the disruption risk is serious enough for emergency action.”

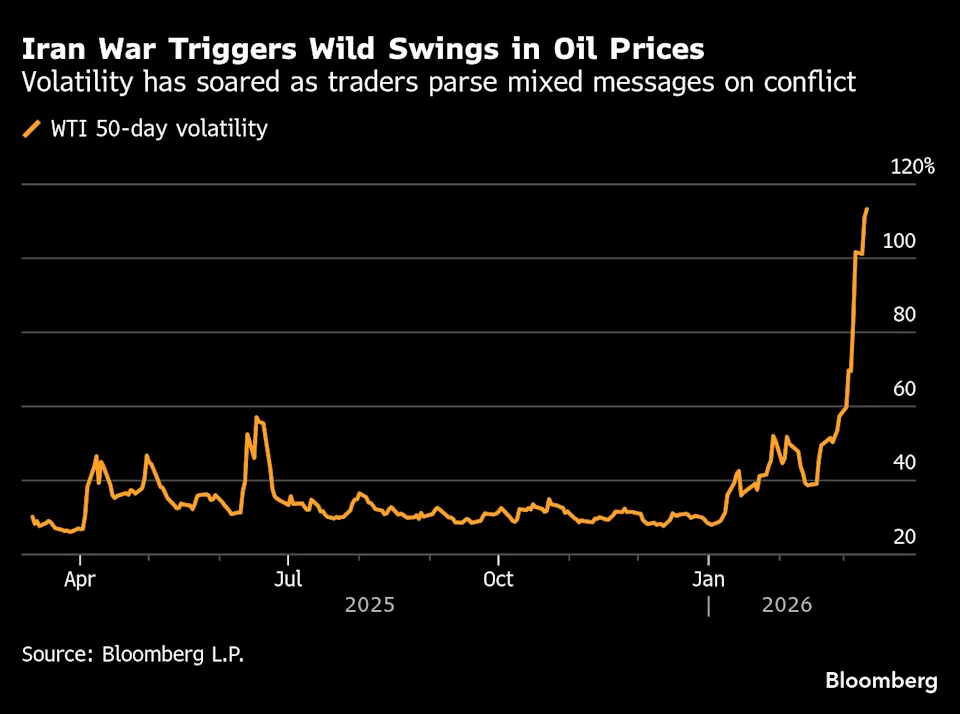

Oil tumbled on Tuesday as the market grappled with rapidly shifting comments from the Trump administration about the war and shipping via Hormuz. Energy Secretary Chris Wright erroneously posted — and then deleted — a message that the US Navy had escorted an oil tanker through the strait near Iran, only for the White House to concede no operation had occurred.

There was also a flurry of conflicting social-media messages from President Donald Trump about mines in the strait. Trump is facing mounting economic and political pressure over the war, and late Monday he said the conflict would be ending soon. However, US officials on Tuesday signaled military operations were escalating and there was little chance of diplomatic talks.

“It very much feels like a market trading in the fog of war, reacting in real time as events unfold,” said Rebecca Babin, a senior energy trader at CIBC Private Wealth Group. “Traders continue to get whipsawed by intense price action and extreme volatility in crude, with headlines driving sharp intraday swings.”

The conflict in the Middle East, now into its second week, has drawn more than a dozen countries into the fray and has sparked concerns about an inflation crisis. US retail gasoline has jumped, putting additional pressure on Trump.

Saudi Arabia, Iraq, the United Arab Emirates and Kuwait have lowered their collective output by as much as 6.7 million barrels a day, or 6% of global output, Bloomberg reported on Tuesday. The biggest oil refinery in the UAE halted operations following a drone strike.

“There would be catastrophic consequences for the world’s oil market the longer the disruption goes on, and the more drastic the consequences for the global economy,” Saudi Aramco Chief Executive Officer Amin Nasser said on Tuesday, his first public comments since the war choked Middle East flows.