rule change means adults 50 and older can now save more than ever")

Tip 1: Have a Plan

Before you start your Spring cleaning, make sure you have a plan. Diving in without a clear path as to what you want to achieve can be tricky.

Your plan should include retirement planning, and may also include other items such as paying off debt, home improvements, college planning, vacation home purchase, etc. we suggest giving thought to what is most important to you and let that dictate your priorities and how you need to plan.

To be successful you will want to implement a disciplined savings schedule. When funding long-term goals, get educated about the different types of financial and investment vehicles available and which are more prudent to utilize for different needs. It’s imperative that you monitor your progress on a regular basis and to make modifications to your plan as events may dictate.

Tip 2: Make a Budget

For many (myself included), the worst thing about Spring cleaning your house is to do a budget. The number of people that plan to retire at a specific age without determining what their income needs will be may surprise you. How do you know your savings goal if you have not calculated how much income you will need in retirement?

Completing a budget worksheet will help you know where your money is going and help you to better plan for retirement.

Tip 3: Know Your Magic Number

How much do you need in savings to sustain your retirement income needs over your lifetime?

Although a budget will help you to determine your regular ongoing expenses: utilities, car payment, insurance, taxes, etc., don’t forget to include any expense associated with what you want to do in retirement.

Retirement is a new phase of your life and hopefully you can enjoy having the time to do the things that bring you happiness. Whether it’s travel, playing golf, dining out, music lessons, arts, boating and so forth, you want to include this in your income needs.

Once you come up with your monthly net figure for needs and wants, deduct how much you will be receiving from Social Security, pension, and any other income sources. Annualize your income needs and multiply by the years you expect to live (just a guess but plan for a long-life expectancy).

It’s best to use a financial calculator that takes into consideration inflation, taxes, average return on investments, or even better, work with a qualified financial professional who can not only help you determine your magic number savings goal but can monitor your plan and help track your progress.

Tip 4: Invest Within Your Comfort Level

Make sure you invest in a way that is appropriate for your comfort level as it applies to risk. Pinpoint your risk number, which you can think of as your sleep number for investing.

There are many risk assessments that you can take to help you determine your comfort level. Ask yourself, “At this stage in my life, what is the maximum risk I can stomach in one year without it changing my retirement outcome?”

Maybe you are two years from retirement and have saved $800,000. If you were to experience a loss of 10% (determine your maximum loss amount), would this affect your retirement?

Even if you are several years from drawing income from your savings, many people are not comfortable with taking on too much risk. Once you have honestly determined how much risk you are comfortable with, match your investments with your individual risk number.

Many financial advisors have tools that can help you with this exercise. Our firm uses a program called Riskalyze to help pinpoint your risk number. Contact us to complete your individual risk questionnaire.

Tip 5: Maximize Tax Efficiency in Retirement

Recognize that taxes may go up in the future. Compared to other time periods, our current tax rates might be considered low.

The U.S. National Debt is over $21 trillion with the two largest budget items being Medicare and Social Security. The massive amount of baby boomers on the verge of retirement was estimated to be 75 million beginning in 2012. Does it occur to anyone what this will do to Medicare and Social Security funding?

Not to mention higher interest is threatening to increase our deficit. The Congressional Budget Office is predicting that rising interest costs will quadruple in a decade or so, rising from $263 billion in 2017 to $965 billion in 2028. Interest payments would become the largest part of the federal budget which will likely hinder the government’s ability to fund programs like Medicare and Social Security.

While you cannot fix the national deficit, you can do proactive tax planning to protect some of your assets from future taxes. Approximately 90% of your federal pension is taxable, up to 85% of your Social Security is taxable, and any distribution from the traditional TSP is fully taxed at your ordinary income rate.

Problems with traditional TSP, 401(k)’s, 403(b)’s, and IRA’s:

- Every distribution is taxed at your highest rate.

- Distributions may put you into a higher tax bracket.

- Distributions often lead to additional tax on your Social Security income.

- Distributions can lead to more tax on capital gains.

- They are the only type of accounts that eventually require distributions, even if you do not want or need the money.

- Highest taxed accounts to leave to heirs.

Roth TSP and IRA

If you are still working, are you contributing to the Roth TSP? If not, why?

As long as you follow the rules: five years have gone by since the year you began contributing to the Roth TSP and you are age 59 ½ or older, your distributions from Roth TSP will be tax-free. While you are working and contributing to the Roth TSP, you will have to pay tax on your contributions, however, your earnings will come out tax-free as long as you follow the rules I just mentioned. The longer you are from retirement, the more you will benefit from tax-free compounded earnings.

The 2018 tax reform legislation signed by President Trump may make Roth Conversions more favorable if you are now in a lower tax bracket. If you are considering converting traditional IRAs and other pre-tax retirement savings into Roth IRA’s, you may never have a better opportunity than now to do it at this historically low tax cost. A Roth conversion done now not only locks in today’s low rates, but also eliminates all the risk of uncertainty regarding how tax rates and rules might change on pre-tax retirement savings in the future.

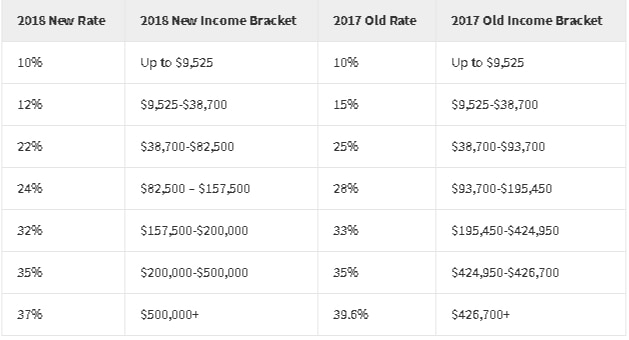

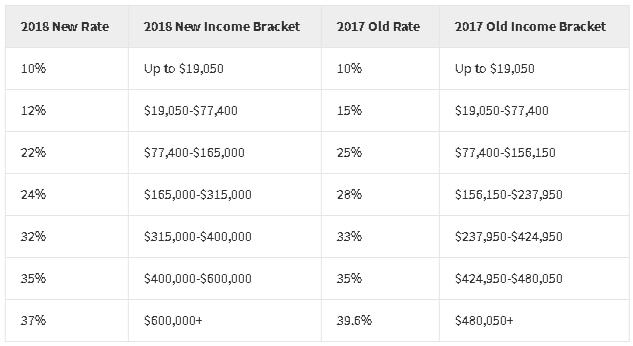

New Tax Brackets

Single Tax Payers

Married Couples Filing Jointly

Please make note that new tax rates sunset after 2025, so if you are planning on doing a Roth conversion or a series of Roth conversions, you should plan on getting that done between 2018 and 2025.

{kind=link}