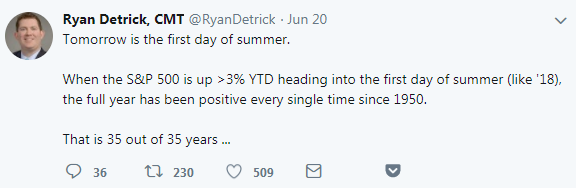

Summer just started and history suggests a sunny forecast. In the 35 times since 1950 when the S&P 500 rose at least 3 percent heading into the first day of the season, the full year was positive every time.

That trend will stretch into a 36th year, according to Mark Tepper, president of Strategic Wealth Partners.

“We’re still overweight stocks at the expense of bonds and we really do expect to hold that positioning at least until the end of the year before we would potentially downshift to neutral,” Tepper told CNBC’s “Trading Nation” on Thursday. “Our research says absolutely no recession until 2020, so it does make sense to stay overweight stocks right now.”

The S&P 500 should end the year at around 2,900, predicts Tepper. Those levels imply a 5.5 percent rise from current levels and would see the S&P 500 end 2018 with full-year gains of 8.5 percent. The benchmark index came close to 2,900 at its record-making peak in late January.

This march to 2,900 won’t be a straight shot, Tepper warns.

“As there’s all this trade war talk going on, as long as that’s a concern, I think the market is going to trade within a range, and I would expect that to really persist through the end of the summer,” said Tepper. “I wouldn’t expect any significant upside until all of this stuff calms down.”

Market fears over a brewing trade war between the U.S. and China have hit stocks this week. The S&P 500 was up just over 3 percent heading into June 21, although it is down 1 percent for the week and on track for its worst week since March. Worries pushed the Dow into negative territory for the year.

Matt Maley, equity strategist at MillerTabak, says the Federal Reserve could introduce larger market tremors than trade worries.

“Every Fed tightening cycle, it has always caused disruptions in the stock market and a slowdown in the economy,” Maley said Thursday’s “Trading Nation.” “It didn’t always cause a recession but it usually did and it didn’t always cause a bear market but it usually did.”

The aftershocks of tighter monetary policy are beginning to be felt on markets, says Maley, and those fissures could widen.

“We saw it in the short-vol trade, then we saw it in emerging markets, and then we saw it in southern Europe, now we’re seeing it in European banks,” said Maley. “Eventually this thing kind of all spills over and eventually hits the U.S. markets, so I’m concerned we’ll see another pullback into correction territory.”

The S&P 500 is currently 4 percent lower than its 52-week high set on Jan. 26, far from the more than 10 percent decline required for a correction. To be at that level, the S&P 500 would need to drop to at least 2,585.

{kind=link}