From sloganeering to Sharm El-Sheikh, sustainability has come a long way, writes Infosys Finacle Europe VP John Barber

It took a long time for sustainability to go from catchy slogans in the streets to a serious conversation in the boardroom. But there is no denying today that sustainability is a front-and-centre consideration for every major corporation, institution and government body worth its salt.

Most recently, the COP27 conference at Sharm El-Sheikh, Egypt added the much-needed push to sustainability, laying out robust frameworks, clear objectives, and firm accountability to be embraced by nations globally.

Even as governments make large moves towards sustainability, their actions will take time to show results. It is industry and commerce that will be able to drive impact much sooner, given their efficiency, productivity, and relative agility when compared to government institutions.

It is heartening to see therefore, that today, most large organisations’ ESG programmes and efforts feature not only in boardroom discussions and coffee table books, but also in annual reports, investor presentations, stakeholder communication, and even in public advertising.

Sustainability actions: banking lags behind

Banks have come under scrutiny in recent times for not doing enough to drive sustainability consciousness within their organisation nor taking a stance through their lending policies to encourage sustainable ways of doing business.

The road to sustainability is a long one that requires patience and perseverance. Banks that work to continuously get better at sustainability, will eventually enjoy the compounded impact of their efforts.

While a lot has already been written about why banks and financial institutions need to lead on sustainability and ESG action in their businesses, this article focuses on immediate action areas that institutions of various shapes and sizes can work on, to build positive sustainability impact, both directly and indirectly, throughout their sphere of influence.

Financial sustainability opportunities within the bank, and beyond

There are two levels of sustainability impact that banks are well-placed to create today. The first is in the implementation of ESG standards and goals within the bank itself. And the second is how the bank’s ESG-consciousness is reflected in its external policies, especially those centered around lending, thereby incentivising the entire ecosystem to be more sustainability focused and creating greater impact in its sphere of influence.

Given the current status of most banks on sustainability action, there are many opportunities for banks to create impact at both levels. A 2021 CDP study revealed that banks’ own emissions are negligible compared to the emissions funded by them. The magnitude of bank-funded emissions can be as high as 700 times the bank’s own emission footprint.

This statistic shines a direct spotlight on the need for banks to not only scrutinise and improve their own sustainability practices but also pay significant attention to the much larger difference they could make by lending better and incentivising sustainable businesses in the economy.

Driving sustainability within the bank

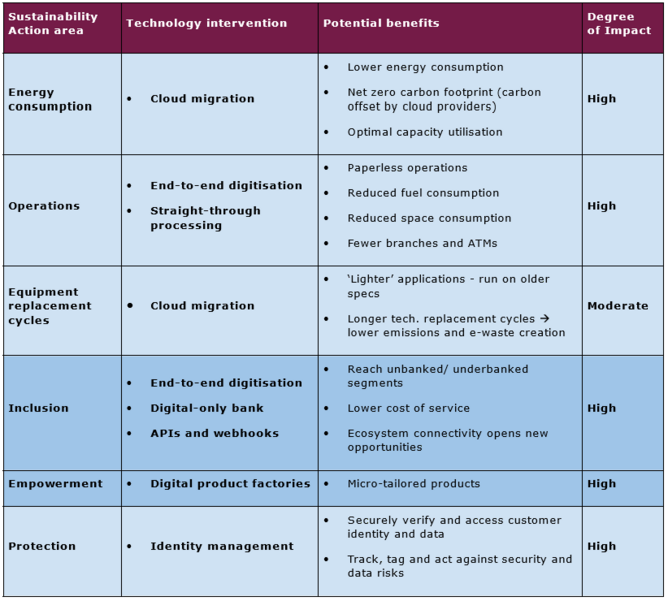

Within the bank’s operations itself, there are several direct and indirect areas where measurement, monitoring, and improvement of sustainability factors could yield significant impact. While each bank’s circumstances, evolution and ESG priorities might differ, there are some ESG action areas that naturally lend themselves to high impact, using technological interventions and digitalisation. Listed below are some sustainability action areas where banks can create significant impact using technology interventions:

Sustainability action areas

Driving sustainability across the bank’s sphere of influence

Beyond addressing its own emissions, a bank can also drive sustainable behaviours in its ecosystem in four different ways:

1. Sustainability through conscious lending

Banks have a unique opportunity to impact sustainable development through lending if they choose to preferentially lend to projects and businesses that align with sustainable development goals.

By funding ‘green’ initiatives and projects, banks not only support the projects themselves, but also contribute to multiple Sustainable Development Goals outlined by the UN, creating an exponential positive impact on the environment and local communities. Listed below are some green lending use cases from banks across the world:

- Green mortgages: The Co-operative Bank in the UK offers green mortgages where a portion of the loan is earmarked for energy-efficient home improvements.

- Energy-efficient auto loans: Wells Fargo in the US offers special financing options for energy-efficient vehicles.

- Solar panel loans: Bank Australia offers better terms on loans for solar panel installations.

- Water conservation loans: TD Bank in Canada offers loans for water-saving home upgrades at lower interest rates and with flexible repayment terms.

- Sustainable agriculture loans: Triodos Bank in Europe offers loans for sustainable agriculture projects with a focus on organic and regenerative farming practices.

- Renewable energy project loans: China Development Bank focuses on lending to renewable energy projects to support China’s transition to a low-carbon economy.

- Eco-friendly home improvement loans: Crédit Agricole in France offers loans for environment-friendly home upgrades such as efficient heating and cooling systems.

- Sustainable business loans: ASN Bank in the Netherlands offers preferential loans to SMEs that are committed to reducing waste, increasing energy efficiency and so on.

- Climate adaptation loans: Yes Bank in India offers loans for communities and businesses to adapt to the impacts of climate change, such as sea-level rise and more frequent natural disasters. These loans can be used for infrastructure upgrades and other measures to enhance resilience.

2. Sustainability through other products and services

Beyond lending, banks can also leverage their wider portfolio of products to encourage sustainable choices amongst customers and reward them for embracing a more sustainable lifestyle. Some examples of such use case are:

- Sustainable investment funds: Goldman Sachs offers its “GS SUSTAIN” funds which invest in companies that are leaders in sustainability and ESG practices.

- Carbon offsetting: HSBC offers a carbon offsetting programme where customers can offset their carbon emissions by investing in renewable energy and reforestation projects.

- Green bonds: European Investment Bank (EIB) is a leading issuer of green bonds that finances projects such as renewable energy and sustainable transportation.

- Energy-efficient credit cards: Bank of America offers a credit card that rewards sustainable choices, such as using public transportation or buying green products.

- Sustainable checking accounts: U.S. Bank offers a “Green Checking” account where for every debit card transaction made using the account, a tree is planted.

- Renewable energy certificates: The JPMorgan Chase Renewable Energy Purchase Programme allows customers to support renewable energy projects through purchase of Renewable Energy Certificates (RECs).

- Sustainable insurance: Swiss Re offers insurance coverage for renewable energy projects and sustainable transportation.

3. Sustainability through ecosystem influence

Banks operate at the heart of commercial and business ecosystems. Along with lending and other offerings, banks can also influence the ecosystem through their actions and policies. Some examples of ecosystem influence are below:

- Corporate Social Responsibility (CSR) reporting: Banks such as Citigroup, DBS, Bank of America and HSBC publish annual reports that provide detailed information on their bank’s sustainability practices and impact. These reports serve as a benchmark on how businesses (especially in financial services) can embrace sustainability profitably.

- Choosing partners and vendors: Banks like BNP Paribas and ING have established sustainability criteria for their suppliers, vendors and partners that include evaluating the environmental and social impacts of their operations and products and encouraging them to adopt sustainable practices.

- Stakeholder welfare programmes: Banks like JP Morgan Chase, Citigroup, HSBC, and Bank of America have built strong stakeholder welfare programmes spanning from health and wellness initiatives to diversity and inclusion to financial wellbeing and affordable housing access.

- Social action programmes: Banks like Société Générale, Barclays, Crédit Agricole and Standard Chartered have a strong focus on community development, with programmes covering areas like youth financial literacy, supporting small businesses and improving representation of underrepresented segments in the financial services industry.

4. Banking can have far-reaching influence on sustainability

Financial sustainability is not just about what banks do to be more sustainable, but also about how banks can influence their entire ecosystem to embrace sustainability as a way of doing business and as a way of life. Banks that lead this charge using technology stand to be leaders in the not-so-distant future.

{kind=link}