We had a crazy jobs week last week, with tons of data that the Federal Reserve was happy to see, but did those labor reports mean we’ve hit peak mortgage rates for 2023? Mortgage rates did fall, purchase application data rose and new listings data came back to trend.

- Weekly active listings rose by only 5,654

- Mortgage rates went from 7.37% and ended the week at 7.08%

- Purchase apps rose 2% week to week

Mortgage rates and the bond market

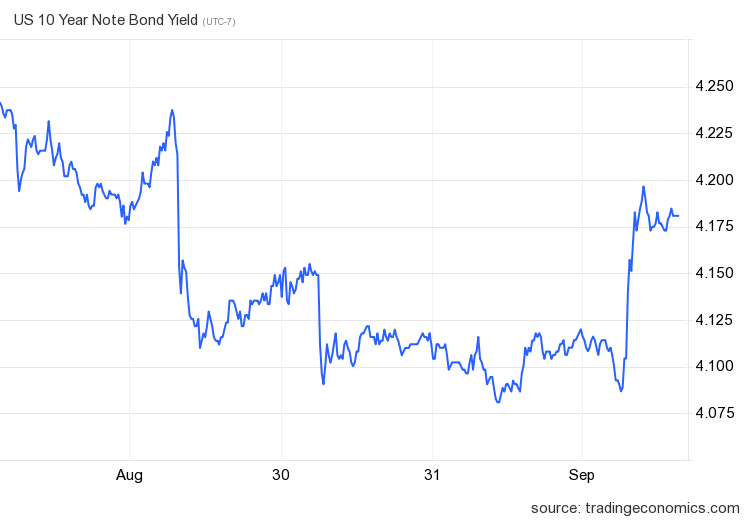

The 10-year yield and mortgage rates were wild last week. Mortgage rates fell from 7.37% to a low of 7.07% and didn’t budge even though the 10-year yield rose on Friday after the jobs report came in. The reason Friday’s pricing was so reasonable was that the spreads between the 10-year yield and mortgage rates were good for a change. So, even though the 10-year yield shot up Friday, mortgage rates only ended up rising 0.01% to 7.08%.

For my 2023 forecast, I had a range of 4.25%-3.21% for the 10-year yield, meaning that rates would be between 5.75%-7.25%. One huge variable change in 2023 was that after the banking crisis started on Feb. 9, the spreads got worse, pushing mortgage rates higher than normal versus the 10-year yield. That, to me, is the big story of 2023, but as we saw Friday, spreads can be a positive story in the future.

Now, after the jobs week, one thing is sure: the labor market isn’t as tight as it used to be. I wrote about this last week as this is a big deal for the Federal Reserve. Since my bond market channel is based on the labor market and the economy, it’s also a big deal for me. Student loan debt payments will hit the economy soon, credit card delinquencies are rising and we no longer have Taylor Swift or Barbie to boost GDP so the economy is slowing down enough to get the labor market even softer.

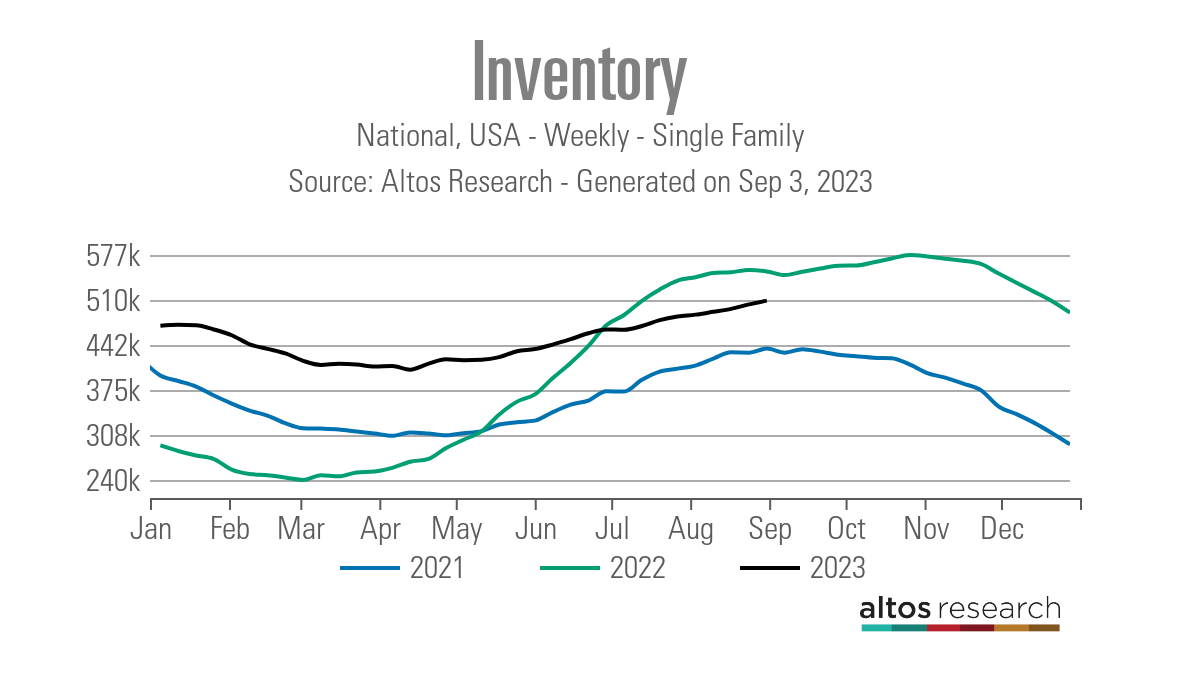

Weekly housing inventory

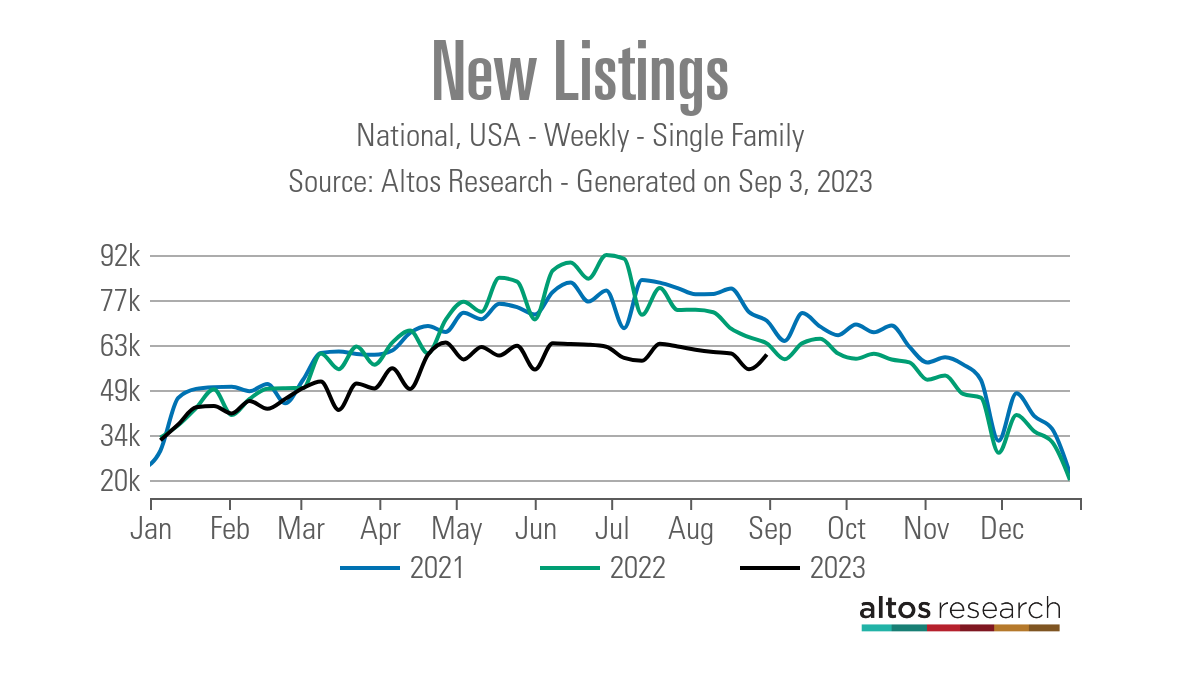

Last week I got a big scare as new listing data fell week to week. We saw a noticeable decline right when mortgage rates rose to their highest point in 23 years, which I talked about on CNBC. However, I only put a little weight on one week’s data, especially near a holiday weekend. Even so, I’m glad we saw a rebound in new listings data last week.

We are still negative year over year and trending at the lowest levels ever for over 12 months. However, we haven’t started a new leg lower in this data line, so we should see flat to positive new listings data soon. New listing data over the past several weeks:

- Aug. 18: 60,295

- Aug. 25: 55,291

- Sept. 1: 60,004

I had hoped for more inventory growth this year, but we haven’t achieved the weekly active listing growth needed for my taste. And we are late in the year as seasonality for active listings traditionally would start its slowdown right now. With that reality, any active listing growth from now on will be a plus in my mind as we start the process for spring 2024.

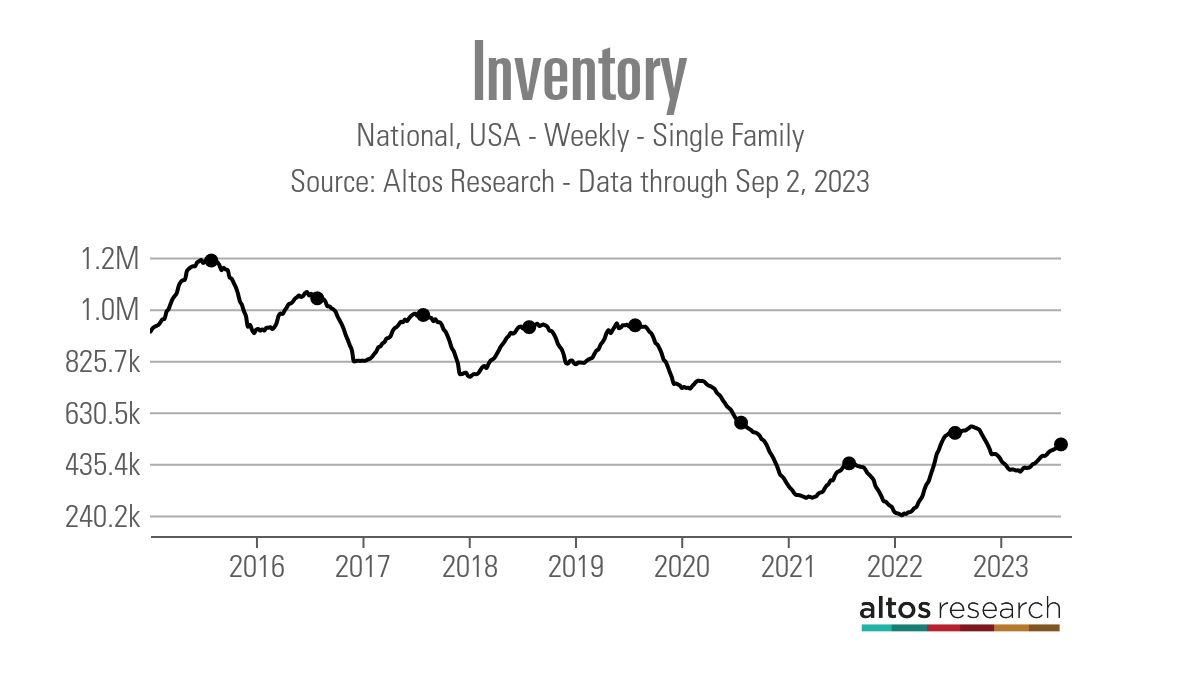

- Weekly inventory change: (Aug. 25-Sept. 1): Inventory rose from 503,159 to 508,813

- Same week last year (Aug. 26-Sept. 2): Inventory fell from 554,748 to 552,536

- The inventory bottom for 2022 was 240,194

- The inventory peak for 2023 so far is 508,813

- For context, active listings for this week in 2015 were 1,205,000

Inventory growth has been slow this year, leading to negative year-over-year inventory since June. We must remember that 2022 had the biggest home sales crash, so the inventory growth was faster than normal.

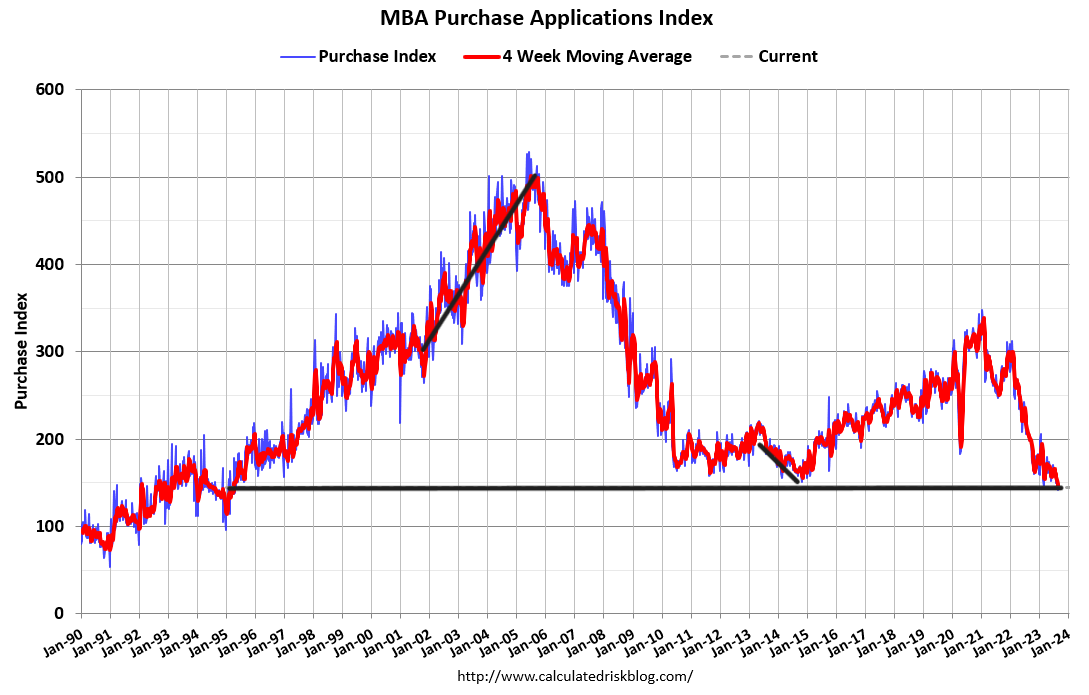

Purchase application data

Purchase application data was up 2% weekly, making the count year to date at 15 positive and 17 negative prints and one flat week. If we start from Nov. 9, 2022, it’s been 22 positive prints versus 17 negative prints and one flat week. While home sales aren’t collapsing like last year, with mortgage rates over 7% the forward-looking housing data has been getting softer.

The week ahead: Bond yields, mortgage spreads and oil prices

Coming off jobs week, which clearly showed a softer labor market, and having the 10-year yield act like it did with better spreads, I am focusing on the bond market and mortgage rates this week. The key for me is the 4.34% level on the 10-year yield. Oil prices are looking to break out, with some credit stress in the system for renters and student loan debt payments coming into play again — that is something to keep an eye on for the economy.

{kind=link}